Opinion of the General Counsel for the National Treasury – Elimination of ICMS from PIS and Cofins tax base

21/06/2021DPC contributes to Subnational Doing Business in Brazil 2021, published by the World Bank

23/06/2021EXPERT OPINION

ECD and ECF: the obligations’ cross-check requires preliminary analysis and technological support to ensure compliance

Technology is essential to ensure the integrity of ECD and ECF data, mitigating risks and ensuring accounting and tax compliance

By André Ferreira

Since the Public Digital Bookkeeping System (SPED) implementation, the cross-checking of information by tax authorities has advanced and become more agile and accurate. As a result, companies had to invest in technological resources to prepare and validate their data. The cross-checking of information between the Digital Accounting Bookkeeping (ECD) and the Tax Accounting Bookkeeping (ECF), specially, has been requiring increased attention from taxpayers.

In May 2021, the Brazilian Federal Revenue Office started a program for notifying more than 58 thousand companies about disagreements found between ECF data and other information existing in its database for 2018 and/or 2019 (read more here). Out of the total number of legal entities that submitted ECF for these years, 3.5% had tax information that indicated economic activities, but revenues from those activities were not included in ECF.

In this case, the federal agency program aims to alert taxpayers to review and correct information spontaneously, without application of fines, until July 12, 2021. The example, however, reinforces that the Federal Revenue Office’s main resource for enforcement actions in the last few years has been the use of technology applied to cross-checking of information.

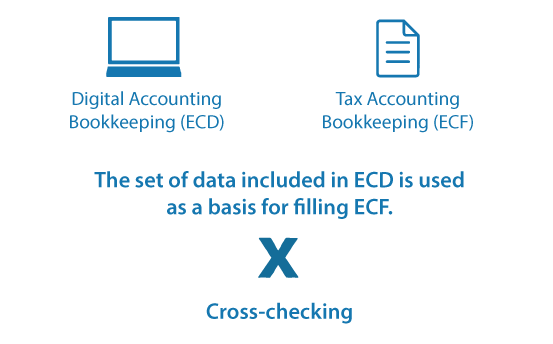

ECD and ECF: what is the connection between these ancillary obligations?

These obligations are complementary, and their information must be aligned.

Below, learn more about these ancillary obligations, about how the information should be treated and how to avoid problems before the Federal Revenue Office after submission, if they have not yet been completed.

- General Journal and its auxiliaries, if any;

- Ledger and its auxiliaries, if any;

- Daily Interim Financial Statements, Balance Sheets and confirming entry forms.

The following books are digitally transmitted through ECD:

On the other hand, ECF includes transactions that influence the composition of the Legal Entity Income Tax (IRPJ) and Social Contribution on Net Profit (CSLL) calculation basis. The digital bookkeeping of the Taxable Income Journal (Livro de Apuração do Lucro Real - Lalur) is mandatory.

Duty

ECD |

ECF |

a) determine a contribution greater than BRL 10 thousand to PIS/Pasep, Cofins and Social Security Contribution on revenue, in accordance to articles 7 to 9 of Act No. 12.546 / 2011, and on payroll; or b) receive revenues, donations, incentives, subsidies, contributions, compensations, insurance, and similar revenues, in a sum greater than BRL 1.2 million. |

All legal entities, including immune and exempt entities, whether taxed based on taxable profit, estimated profit or presumptive profit, are required to submit ECF, except:

|

Deadlines

According to the rules, the obligations follow the schedule below:

ECD |

ECF |

|

Last working day of May in the year after the calendar year. |

Last working day of July in the year after the calendar year. |

Deadlines in 2021

In 2021, due to the pandemic, the deadline for submitting the ECD for the calendar year 2020 was postponed to the last working day of July (07/30). Similarly, ECF submission is expected to be delayed, but there is still no official government publication confirming change of deadline for submitting the tax bookkeeping.

Preliminary analysis

Together, ECD and ECF require a large amount of information from the taxpayer, and these obligations are also cross-checked with other ancillary obligations. For that reason, maintaining a well-coordinated accounting and tax routine is the best path to ensure compliance.

Throughout each year and for complying with current legislation and requirements, preliminary analysis has an essential role of validating entered information for flawless consolidation.

Advantages for taxpayers in conducting preliminary analysis:

Technologies for reviewing and cross-checking ECD and ECF

A secure accounting and tax management also includes the use of specialized technology to cope with the technological apparatus used by the tax authority when performing cross-checking.

Today, in order to ensure compliance of obligations and reduce the risks of committing failures that may result in penalties, it is necessary to use softwares that validate information and simulate cross-checking, as a way of preventing inaccuracies.

Precautionary review is essential for filling records correctly, since it prevents omissions and data divergence between files.

The programs used in the verification process must be parameterized and aligned with the tax requirements for ensuring data processing quality, in a way to execute validations before formal sending.

Taxpayers who have already submitted ECD and ECF, can perform a corrective analysis, anticipating possible identification of inconsistencies by the tax authorities.

For example, if inconsistencies are identified when preparing ECF and the ECD has already been delivered, it may be necessary to rectify the submitted bookkeeping.

It is also necessary to check if information included in the ECF is aligned with other ancillary obligations, such as DCTF, DIRF and EFD Contribuições.

Since this whole process involves a large amount of data, relying on the use of technological tools that promote these assessments is essential in the SPED era we live in.

Technology for compliant submission

Domingues e Pinho Contadores has a consulting and operational team ready to advise taxpayers and carry out the annual submission of ECD and ECF. DPC analyzes and operates parameterized systems in accordance with the tax authorities' requirements, ensuring efficient management of submissions. As a result, clients can feel secure and confident in relation to these processes.

In addition to routine customer service, DPC offers consulting services in a case-by-case basis, guiding taxpayers concerning the need for adjustments and rectifications.

Author: André Ferreira, partner at Domingues e Pinho Contadores.

How DPC may help your company?

Domingues e Pinho Contadores has specialized team ready to assist your company.

Contact us by the e-mail dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318