Brazilian Federal Revenue Office and National Treasury Attorney-General’s Office (PGFN) sign a public notice acceding to the agreement of tax litigation transaction

20/05/2021CGSIM – Addresses simplification measures and provides for the operational model of entrepreneur and legal entity registration and legalization

21/05/2021EXPERT OPINION

Elimination of Tax on Goods and Services (ICMS) from PIS/Cofins calculation basis: from courts to credit setoff or refund

New tax scenario creates tax opportunities for medium and large companies

By Rita Araújo

The Supreme Federal Court (Supremo Tribunal Federal - STF), in a historic decision, on May 13, has established that the Tax on Goods and Services (Imposto sobre Circulação de Mercadorias e Serviços - ICMS) indicated on the tax document must not be included in the calculations of Social Integration Program Contributions (PIS) and Social Security Financing Contribution (Cofins). This decision benefits taxpayers who claim at courts, as the exclusion has great potential to create positive impacts on companies' cash.

STF decided that the exclusion of ICMS from the PIS/Cofins calculation basis will take effect as of March 15, 2017.

This decision caused great upshot in the market, as it opens opportunities for businesses to recover tax credits. The measure can move significant sums, depending on the quantity of operations accomplished during the period that will be included in the analysis.

At the moment, companies must organize themselves and seek advisory support to take assertive decisions in face of the new tax scenario.

ICMS and PIS/Cofins: understanding what has changed

ICMS is a type of value-added tax, within the jurisdiction of each State and the Federal District that is levied on the selling of goods or on the rendering of telecommunication services and intercity or interstate transportation services. Its rate varies in each jurisdiction, according to the good or service, and can range from 7% to 35%, with most rates varying between 17% and 19%.

On the other hand, the Social Integration Program (Programa de Integração Social - PIS) and Social Security Financing Contribution (Contribuição para o Financiamento da Seguridade Social- Cofins) are social contributions at Federal level, applied on invoicing - in case of cumulative calculation tax regime - and on total revenue earned by the legal entity, regardless of its denomination or accounting classification - in case of non-cumulative calculation.

According to the law, without support of a court decision, PIS/Cofins contribution rates are applied on the base value, including ICMS.

What changes is that there will be no more tax on tax charge, triggering the ICMS exclusion on PIS/Cofins calculation basis. For the benefit of taxpayers, this will put an end to the snowballing nature of these taxes, reducing the amount to be paid.

Actions to be taken by companies

The possibilities are the following:

Businesses impacted by the decision

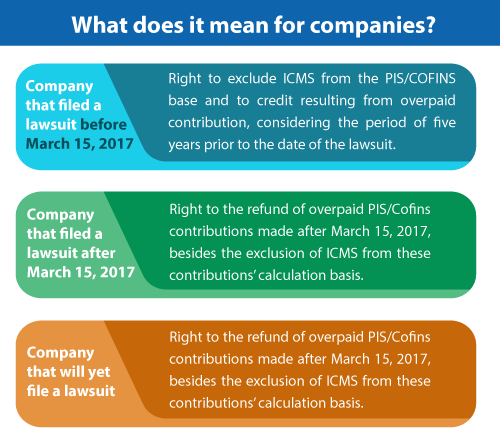

The STF decision, which links all lawsuits related to the topic at hand, is important for both medium and large businesses, regardless the segment - industry, sales or services - which have significant ICMS tax burden on their operations. Companies can file a lawsuit to claim their rights, not paying PIS and Cofins under ICMS on their daily transactions and receive what they have overpaid, limited to retroaction to March 15, 2017.

Recovering credits in practice

First of all, it is important to analyze the cost-benefit of filing a lawsuit. Thus, it is recommended that the company get expert tax support, in order to calculate the savings beforehand, including the amount to be reimbursed, from 03/15/ 2017.

Having filed the lawsuit and after the lawsuit is completed, regarding the use of credit resulted from overpayment after 03/15/2017, the credit authorization must be requested, via administrative procedure at the Federal Revenue Department. Subsequently, tax refund or tax compensation must be requested via PER/DCOMP.

DPC's experts help business opportunities seek

Domingues e Pinho Contadores offers support to businesses that want to benefit from this legal decision, either in cases where there is ongoing lawsuits or in situations where the company has not yet acted judicially.

DPC experts analyze the company's tax performance, identifying opportunities for applying for tax credits, either from routine monitoring or from a survey done for a specific case.

In order to deliver a complete solution to the customer, DPC technology team acts to ensure the correct tax bookings and tax credits calculated by updating setup calculations in the tax system.

Author: Rita Araújo, partner and director at Domingues e Pinho Contadores.

How DPC may help your company?

Domingues e Pinho Contadores has specialized team ready to assist your company.

Contact us by the e-mail dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318