Expatriates: companies must be aware of issues related to payroll and income tax

20/09/2021Provisional Measure No. 1.046 of 2021 – End of term

23/09/2021EXPERT OPINION

Exclusion of ICMS from PIS/Cofins tax base: clarifications on credit offset and refund

Offset and/or refund of credits from March/2017 to June/2021 can be carried out without a lawsuit

By Rita Araújo

The Federal Supreme Court (Supremo Tribunal Federal - STF) concluded, in May 2021, the so-called "thesis of the century", which determined that ICMS should not be part of the PIS/Cofins tax base. It was also defined at the time that the ICMS considered for exclusion is the one indicated in the invoice and that the effects are valid as from 03/15/2017.

The measure has great potential to produce positive impacts on companies' cash. The savings can be significant, depending on the business' income, the State where it is located, and the tax regime adopted.

Since STF's decision, other complementary disclosures of government agencies have been adding new chapters to the issue. The National Treasury Attorney-General's Office expressed its opinion through Opinion SEI No. 7698/2021 and the Federal Revenue Office complied with the determination of this act, disclosing on 06/24/2021 the amendment to the Practical Guide 1.35 of EFD-Contribuições, with specific instructions about the procedures for ICMS exclusion from PIS/Cofins tax base.

Which companies can benefit right away?

Taxpayers taxed by Real Profit or Presumed Profit who sell goods and/or providers of telecommunication and intercity or interstate transport services that have not filed a lawsuit related to the matter.

Companies opting for Simples Nacional, therefore, cannot adopt the measure.

How to adopt the procedure for not including ICMS in PIS/Cofins tax base?

Since the Federal Revenue Office's update in the Practical Guide 1.35, published on June 24, 2021, taxpayers can exclude ICMS from PIS and Cofins tax base, issuing the invoice indicating the tax base value without ICMS.

How to use the overpaid amount?

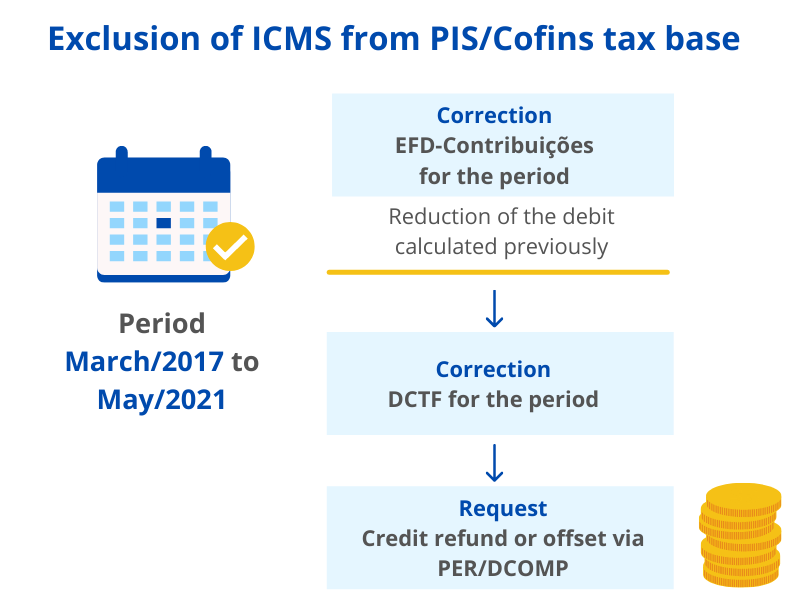

To use as offset or request refund of amounts overpaid since March 15, 2017, taxpayers must correct EFD-Contributions, month by month and item by item, continuously determine the new value of the Contributions, and correct DCTF.

The installments overpaid after these procedures will be subject to a request for refund and/or offset via PER/DCOMP.

It is worth considering that the process involves many adjustments of fields and information. Thus, it is essential that the work is carried out attentively and by a specialized professional to avoid failures.

What are the risks?

Mistakes can result in penalties of at least 50% over the wrongly offset debt. Hence the need to rely on specialists to carry out the calculations and corrections.

What happens to taxpayers who have already filed a lawsuit?

Taxpayers with ongoing lawsuits must wait for it to become final.

Expert guidance

Domingues e Pinho Contadores can assist your company in raising tax credits, making necessary adjustments and requesting offset/refund via PER/DCOMP.

Specialized support also helps in more strategic decisions related to tax opportunities, always with a customized service considering each client's business goals.

Author: Rita Araújo, partner and director at Domingues e Pinho Contadores.

How may DPC help your company?

Domingues e Pinho Contadores has a specialized team ready to assist your company.

Contact us by email at dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318