The Federal Revenue has extended the deadline for reporting the Income Tax Return

15/04/2021DPC supports Trimble to overcome the integration challenges in the merger process

19/04/2021HIGHLIGHTS

Income Tax Return: precautions to prevent the risk being caught in the malha fina

Knowing the main inaccuracies that lead to a pending at RFB helps to prevent problems with the tax authorities

Inattention to the rules and carelessness when filling out the income tax return can cause problems. Simple errors or omissions can lead the taxpayer to be caught in a RFB detailed audit or, as popularly said malha fina* (a Brazilian expression that is explained as a detailed audit to identify inaccuracies in the information reported to the RFB).

More and more effectively, the information presented to the agency is electronically verified. This verification is immediate, started as soon as the report is received, and considers information presented by third parties, such as companies, financial institutions, and health assistance providers.

If there is any inaccuracy between what is reported in the statement and the information provided by other parties, the system immediately segregates the tax return for a more detailed analysis and the DIRPF is retained in the inspection.

“There are situations in which the statement gathers few information. But there are also taxpayers with many sources of income, goods, who have made purchases, sales, and investments in Brazil or overseas. In these cases, it is necessary to redouble the attention to a compliant filing”, warns Augusto Andrade, leader of the Individual ‘s Department at DPC.

In the last year, at the end of the processing period, the RFB reported that 910,996 taxpayers had their tax return retained. The number corresponds to 2.74% from total of transmissions, which, in the last financial year, it was over than 33 million of documents sent.

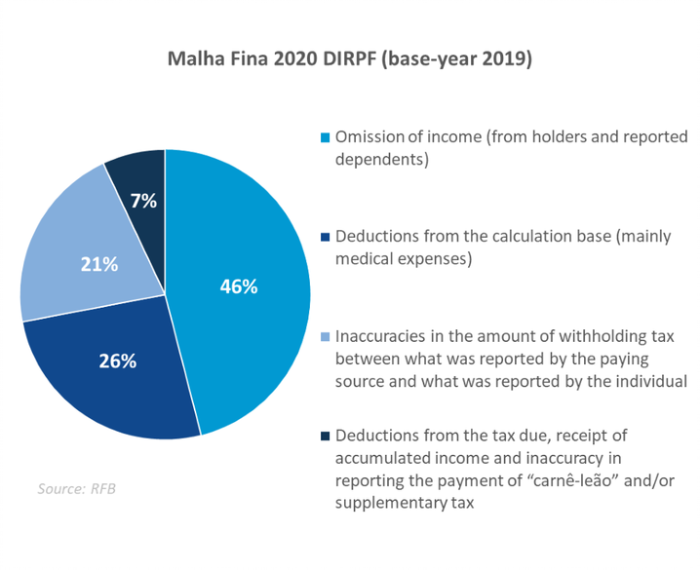

Knowing the main inaccuracies that lead to the RFB audit helps in preventing problems with the Tax Authorities. See the main causes in the last year:

For taxpayers not being among the cases in this new year, some precautions must be taken. Andrade recalls that organization is also an ally.

“By dedicating time to gather documentation and clarify topics that have raised doubts, the taxpayer avoids mistakes that could lead to be caught in the RFB audit".

Avoiding the malha fina: highlights

Wrong and divergent values

In addition to devoting time to fill the form, the taxpayer must review it before submitting. Typing errors or entering values in incorrect fields are easily identified by a data-crossing.

Informing values in the taxable income form different from those provided by the paying sources is a fault easily identified by the system and the one that most leads to the retention of the declaration.

Inclusion of dependents

Firstly, the taxpayer should observe the criteria for classifying dependents. Some taxpayers attempt to include expenses with relatives who do not qualify for the dependency relationship, which is considered a failure.

Another situation that raises doubts is the inclusion of children from separate parents. The dependent, in this case, must be listed in the guardian's report. When there is shared custody, it is necessary to reach an agreement so that the dependent is in only one tax return.

It is important to keep in mind the rule that a dependent's CPF must not appear on more than one tax return. Thus, when two taxpayers share the expenses of children, parents, or grandparents, the family must align who will be responsible for reporting for deducting expenses.

When included in the report, the dependent also “brings” the income, assets, rights and debts. This includes gains related to the internship scholarship and alimony, for example.

Alimony

While income, alimony is taxable and must be reported by the holder of the statement, even if the pension is payable to a dependent.

Those who pay a pension registered in a judicial agreement can deduct 100% of the taxable income.

Medical expenses

According to the rules, health expenses can only be deducted when they are made for their own benefit or for dependents, upon proof by means of notes and receipts. The proofs must have the health professional's signature, name, CPF (Individual’s Taxpayer Number) and patient data.

Listing medical expenses with values other than receipts and not informing the amount reimbursed is a quite common mistake that has led taxpayers to have the statement retained.

Education expenses

The deduction of expenses of the taxpayer and dependents is only allowed for children's, elementary, high school, and college tuition, including university, master's, doctorate, and specialization courses. Furthermore, there is a deduction limit for this expense: BRL 3,561.50 per registered person.

Daycare expenses, language, and other extracurricular courses are not deductible.

Rent expenses and income

Both those who receive and those who pay rent must list the earnings/payments in the statement. The rent gains are taxable and must be reported. The expenses are not deductible.

Gains on shares

If the total value of the sale of shares on the stock exchange in Brazil exceeds BRL 20,000 in a month, the taxpayer will be taxed on the net profit of the operations.

Profits from day trade operations (buying and selling on the same day) and Real Estate Funds generate income tax on any operation, regardless of the total amount of sales for the month. In this case, the tax rate is 20% on income.

See also: Taxation on investments: individuals should analyze the effects of taxes on profitability

Rely on experts and avoid the risk of going through the malha fina

Supported by DPC, the taxpayer can have peace of mind about completing the tax return, especially when this obligation involves special, more complex situations, eliminating the risk of having the return filed after the deadline or being caught by the inspection due to inaccuracies or omissions.

How DPC may help you?

Domingues e Pinho Contadores has specialized team ready to assist you.

Contact us by the e-mail dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318