Management of cash flow: alternatives to minimize the crisis effects

08/07/2020FGTS installments plan: DPC supports clients to overcome difficulties in issuing and payment of payment slips

10/07/2020HIGHLIGHTS

ISS-RJ: Tax incentive to culture can minimize the effects of Covid-19 in the city of Rio de Janeiro

Companies have the opportunity to keep the city's artistic production active and also generate benefits for the institutional image

Private initiative has always played an important role in supporting and strengthening the cultural sector. At such moment, bringing more companies to contribute to the local culture is a way of increasing the value of this segment and helping the artistic class to overcome the effects of the crisis triggered by the Covid-19 pandemic.

In the city of Rio de Janeiro, through the Municipal Law for Incentive to Carioca Culture - Law 5553/2013, it is possible to support projects that will work to keep art alive and in motion.

This law provides that corporate taxpayers may encourage cultural projects by allocating up to 20% of the ISS due to the municipality.

More than ever, in this challenging scenario, the company has the opportunity to keep active the artistic production of its city, contributing to quality art, education and entertainment reaching more people, especially those who have less access.

Promoting culture, especially at this time, is also a way of putting the business' social responsibility policy into practice, reinforcing corporate citizen action and generating positive effects to the brand.

ISS-RJ: how does it works

To make the support feasible, it is necessary to register with the city hall of Rio as an incentive contributor (sponsor).

The supporting company then selects one or more projects from among those registered with the city hall by the cultural producers that year and passes on up to 20% of the amount related to ISS due to the municipality to the selected initiative(s).

The payment that will be intended to the cultural project is made in the same tax payment form, the Municipal Revenue Collection Document (“DARM”), issued through “Nota Carioca” portal.

On the other hand, the companies that provide incentives may receive benefits to be reversed to their employees, clients or to the community. This opens the way to work on aspects related to the positive strengthening of the brand with these groups.

There are 19 areas to choose from: visual arts, crafts, audiovisuals, libraries, cultural centers, cinema, circus, dance, design, folklore, photography, literature, fashion, museums, music, multiplatform, theater, transmedia, preservation and restoration of natural, material and intangible heritage.

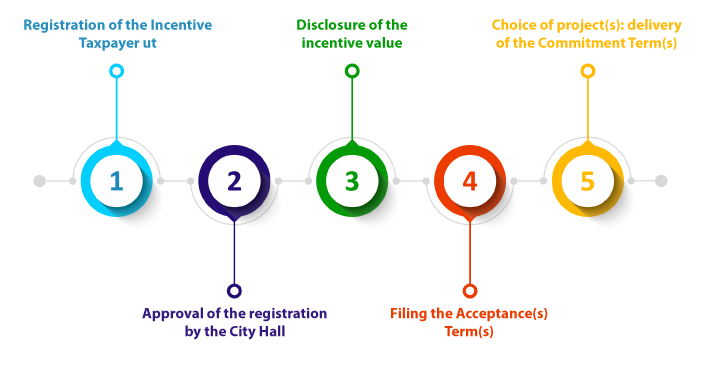

Learn the steps of the process:

1. Registration of the Incentive Taxpayer

All legal entities that are taxpayers of the Tax on Services (ISS) in the municipality can register, except for:

- Micro and small companies, opting for Simples Nacional.

- ISS taxpayers whose tax is fully withheld by the service user, under the terms of Law 691/84.

- Companies that exclusively pay ISS as a taxable person, under the terms of Law 691/84.

2. Approval of the registration by the City Hall

The registration, when in compliance with the notice, the it is approved. If the company is considered ineligible at this stage, it is possible to appeal.

3. Disclosure of the incentive value

In this stage, the City Hall discloses the proportionality result and the total amount of the taxpayers’ tax incentive.

The total interest limit is 20% of the company's ISS payment, based on the previous fiscal year. However, this percentage may not be reached. The law establishes a tax waiver of at least 1% of the ISS collected by the city in the previous year.

If the amount informed by the sponsoring taxpayer companies exceeds this amount, the proportionality formula will be applied, and then the amount available will be prorated among all registered and qualified companies.

4. Filing the Acceptance(s) Term (s)

By means of the Acceptance Term, the incentive taxpayer confirms to the Municipal Treasury Secretariat its intention to encourage cultural projects, considering the values approved by the City Hall.

5. Choice of project (s): delivery of the Commitment Term (s)

It is through the Term of Commitment that the taxpayer commits to directing the ISS for a specific project. It is at this moment that the company makes the choice.

The incentive taxpayer has at disposition hundreds of cultural projects, previously approved by the Municipal Secretariat of Culture and qualified to receive sponsorship.

The sponsor should pay attention to ensure that the project has to capture at least 30% of the total approved in sponsorship. Otherwise, the City Hall will not transfer the funds and, therefore, it will not be feasible.

Deadlines

- Supporting taxpayers will have from August 1 to 31, 2020 to apply.

- As a rule, the disclosure of the result with qualified taxpayers occurs up to October 15.

- Producers and taxpayers must send the Commitment Term(s) between November 1 and December 15 (catchment period).

These deadlines were presented by the City Hall's Municipal Department of Culture. However, it is important to monitor whether the schedule will change due to the coronavirus pandemic.

Culture incentive with specialized guidance

In addition to the negotiated offsets, the incentive creates possibilities for many institutional image gains. Companies that want to support the selected projects and benefit from the culture incentive legislation in the municipality of Rio de Janeiro can find specialized guidance with Domingues e Pinho Contadores.

The DPC team supports the legal entity from registration as an incentive taxpayer, in accordance with the public notice, through the following procedures and stages, including directing the allocation of ISS resources throughout the implementation year.

How DPC may help your company?

Domingues e Pinho Contadores has specialized team ready to assist your company.

Contact us by the e-mail dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (22) 2773-3318