Released Contribution Salary Table and Update Factors for Benefit Calculation

14/01/2025End of Dirf: What Changes for Companies

24/01/2025HIGHLIGHTS

Tax Reform Enacted: What Changes and How the Transition Will Work

Taxpayers Must Adapt to the Impacts of the New Brazilian Tax System

On January 16, through Complementary Law No. 214/2025, the Tax Reform was enacted, establishing a fiscal milestone in the country and a new taxation system for goods and services. A gradual transition will begin in 2026, with full implementation by 2033.

With this regulation in place, Brazilian business owners and taxpayers must prepare for a period of transformations and reassessment of practices to maintain competitiveness and ensure tax compliance. As with any change, challenges and opportunities are involved.

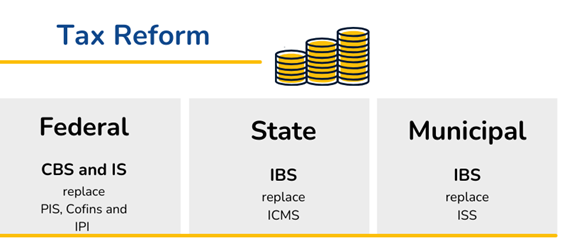

New Tax System

With the Tax Reform, Brazil will adopt a IVA Dual (Value-Added Tax) system, composed of: CBS (Contribution on Goods and Services) at the federal level and IBS (Tax on Goods and Services) at the state and municipal levels.

A new federal regulatory tax, the Selective Tax (IS), is also being introduced to discourage the consumption of products deemed harmful to health and the environment. Known as the "sin tax," the IS imposes a higher tax rate than the standard rate. Among the items subject to this additional tax are cigarettes, sugary and alcoholic beverages, boats and aircraft, cars (including electric vehicles), physical and online betting, and the extraction of iron ore, oil, and natural gas.

The restructuring requires companies to understand new tax concepts, calculate differentiated rates, and adjust their internal processes.

It is worth noting that the new taxes will have rates defined by complementary legislation.

According to the enacted text, the CBS and IBS rates will be set by specific legislation. The federal government will set the CBS rate, while each state and municipality will set its IBS rate. Reference rates, in turn, will be established by a resolution of the Federal Senate.

Transition

During the transition period, the old tax system will coexist with the new one. This means that companies will have to operate on two fronts simultaneously: collecting current taxes while adapting to the implementation of the new ones. This overlap increases operational complexity during this phase.

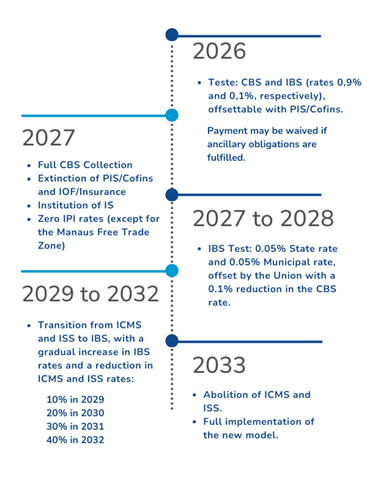

In 2026, with the start of the system’s implementation, there will be no actual collection of new taxes, but rather a "test rate."

In 2027, the Selective Tax will come into effect. The federal CBS will be effectively collected, and the following taxes will be abolished: PIS and Cofins, IOF/Seguros, and IPI exemption (except for industrialized products in the Manaus Free Trade Zone).

The IBS will have a longer implementation period, with four years of coexistence with ICMS and ISS.

The transition will conclude in 2033, when IBS and CBS will be fully implemented.

Other points

Another innovation is the cashback system, which provides for the refund of part of the tax paid to taxpayers. This measure benefits individuals from low-income families.

The text also establishes a list of tax-exempt food and medicine. Additionally, other food and medicine items have been included in the reduced 60% tax rate. This same reduction percentage applies to education and healthcare services, medical devices, accessibility devices for people with disabilities, artistic, cultural, event, journalistic, and audiovisual productions, among other items.

Furthermore, 18 activities performed by self-employed professionals will have a 30% reduced tax rate, including administrators and lawyers.

How to deal with challenges

The new tax scenario will require an understanding of the new guidelines, combined with the ability to operate adapted systems to minimize risks and errors.

The transition phase will be marked by regulations defining details on tax rates and exceptions. Companies will have the challenge of constantly keeping up with regulatory changes in order to operate under current rules.

Seeking specialized support and adopting technological solutions for tax management will be a key factor in dealing with the complexity of the transition.

Tax intelligence

With teams and offices in Rio de Janeiro and São Paulo, DPC develops tax solutions aligned with the specificities and needs of each client, ensuring a complete approach in full compliance with the legislation and tax reality in force. Count on this support: dpc@dpc.com.br.

How can DPC help your company?

Domingues e Pinho Contadores has a specialized team ready to assist your company.

Contact us at dpc@dpc.com.br

See more

Sign up for our Newsletter:

Are you interested?

Please contact us, so we can understand your demand and offer the best solution for you and your company.

Rio de Janeiro

Av. Rio Branco 311, 4º e 10º andar - Centro

CEP 20040-903 | Tel: +55 (21) 3231-3700

São Paulo

Rua do Paraíso 45, 4º andar - Paraíso

CEP 04103-000 | Tel: +55 (11) 3330-3330

Macaé

Rua Teixeira de Gouveia 989, sala 302 - Centro

CEP 27910-110 | Tel: +55 (21) 3231-3700/p>